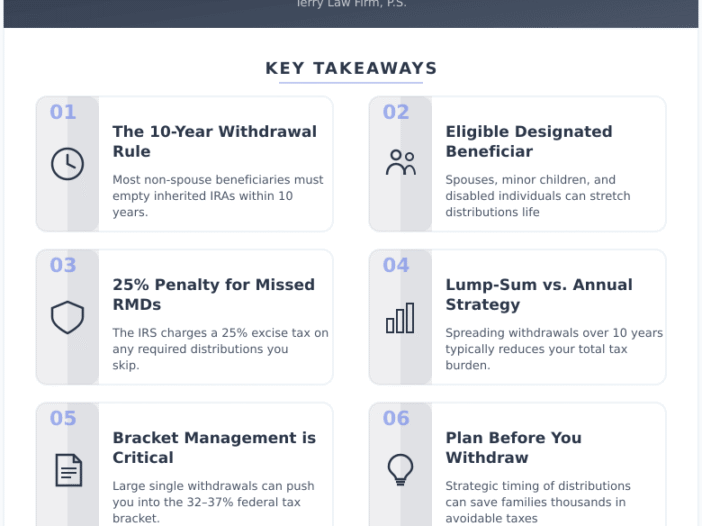

Inheriting an IRA triggers federal tax rules that catch most families off guard. The 10-year rule, introduced by the SECURE Act, requires most non-spouse beneficiaries to fully withdraw inherited IRA funds within a decade – and depending on when the original owner started taking distributions, annual withdrawals may also be required along the way. Missing these deadlines carries a 25% IRS excise tax penalty. Washington State residents have a meaningful advantage: no state income tax, meaning distributions are only taxed at the federal level. Smart distribution planning – spreading withdrawals across low-income years rather than taking a lump sum – can save families thousands. This guide covers who qualifies for the 10-year rule, how traditional and Roth inherited IRAs differ, Washington-specific tax context, and the most common mistakes beneficiaries make before speaking with a legal or tax professional.

Terry Law Firm

PLAN FOR YOUR FUTURE AND PROTECT YOUR LEGACY

Footer

Washington

15306 Main St E, Ste B

Sumner, WA 98390

Phone: (253) 299 6800